HEALTH INSURANCE MONTHLY PREMIUM

HEALTH INSURANCE MONTHLY PREMIUM

Health insurance monthly premium is one of the most searched topics today as medical costs continue to rise across India. Whether you're buying insurance for the first time or planning to switch your policy, understanding how monthly health insurance premiums work can help you save money while getting maximum coverage.

In this detailed guide, we explain what health insurance monthly premium means, how it is calculated, factors affecting pricing, how to reduce premiums legally, and how to choose the best medical insurance plan based on your budget.

What is Health Insurance Monthly Premium?

Health insurance monthly premium is the amount you pay every month to keep your medical insurance policy active. Instead of paying the full annual premium in one lump sum, insurers allow you to pay in monthly installments, making health coverage more affordable and accessible.

Your monthly premium ensures:

- Continuous medical coverage

- Cashless hospitalization access

- Protection against rising healthcare expenses

- Financial security during medical emergencies

In simple words, your health insurance monthly premium is the cost of peace of mind for your family’s healthcare needs.

Why Health Insurance Monthly Premium Important?

Many people delay buying health insurance because of budget concerns. Monthly premium payment options solve this problem by spreading the cost over 12 months instead of one large annual payment.

Key benefits of monthly premium health insurance plans include:

- Easy on monthly finances

- No compromise on coverage

- Better cash flow management

- Continuous medical insurance protection

- Reduced financial burden during emergencies

With hospitalization costs crossing ₹5–10 lakhs for major treatments, paying a small monthly premium for health insurance can save your lifetime savings.

Factor Affecting Health Insurance Monthly Premium

Your health insurance monthly premium depends on several factors. Understanding these helps you choose the best plan at the lowest cost.

1. Age of the Insured

Higher age = Higher premium. Younger policyholders enjoy lower monthly health insurance premiums.

2. Sum Insured Amount

Higher coverage leads to higher premiums. For example, a ₹10 lakh medical insurance policy will cost more than a ₹5 lakh plan.

3. Medical History & Pre-existing Diseases

People with diabetes, hypertension, or heart conditions usually pay higher monthly premiums due to increased risk.

4. Type of Policy

- Individual health insurance plans

- Family floater medical insurance plans

- Senior citizen health insurance plans

- Critical illness insurance plans

Each category has different premium structures.

5. City of Residence

Metro cities like Mumbai, Delhi, Bangalore, and Chennai have higher hospital costs, which increases health insurance monthly premium rates.

6. Add-ons and Riders

OPD cover, maternity benefits, room rent waiver, critical illness riders, and personal accident riders increase your monthly insurance premium.

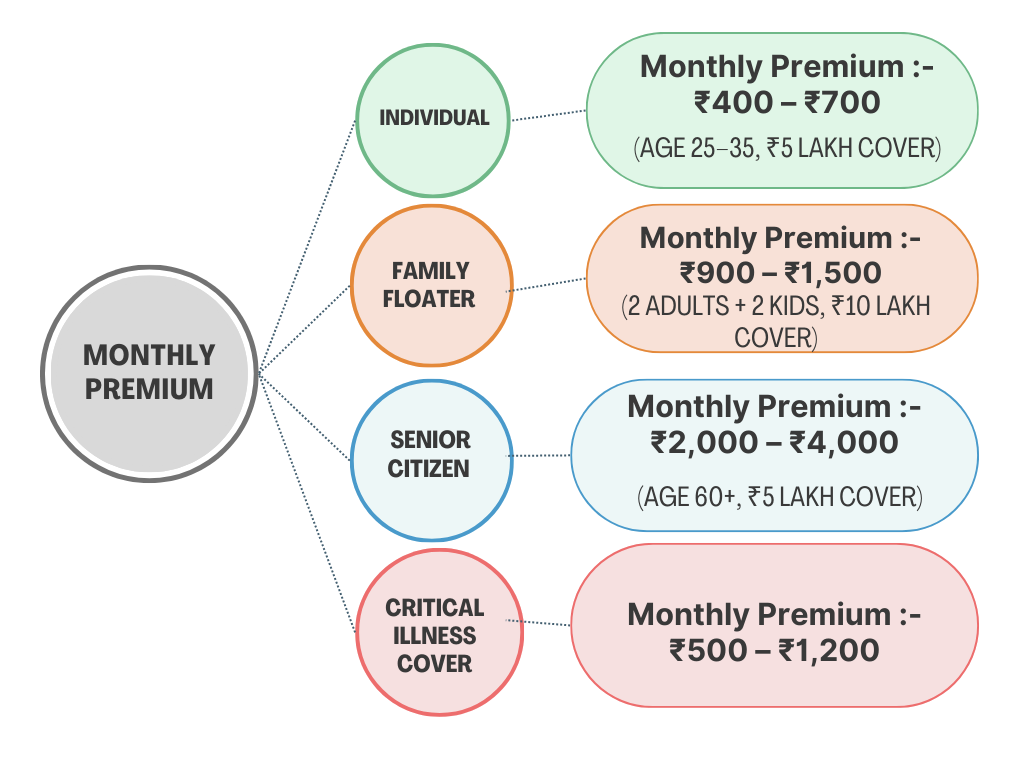

Average Health Insurance Monthly Premium In India

Health insurance premiums in India vary based on several factors such as age, sum insured, family size, medical history, and the type of coverage selected. Younger individuals usually pay lower premiums, while senior citizens and higher coverage plans cost more. Choosing the right plan helps you balance affordability with adequate protection. Below is an estimated monthly premium range for different profiles to give you a general idea:

Here’s an estimated monthly premium range in India

Actual health insurance monthly premiums depend on insurer, coverage, medical history, and benefits selected.

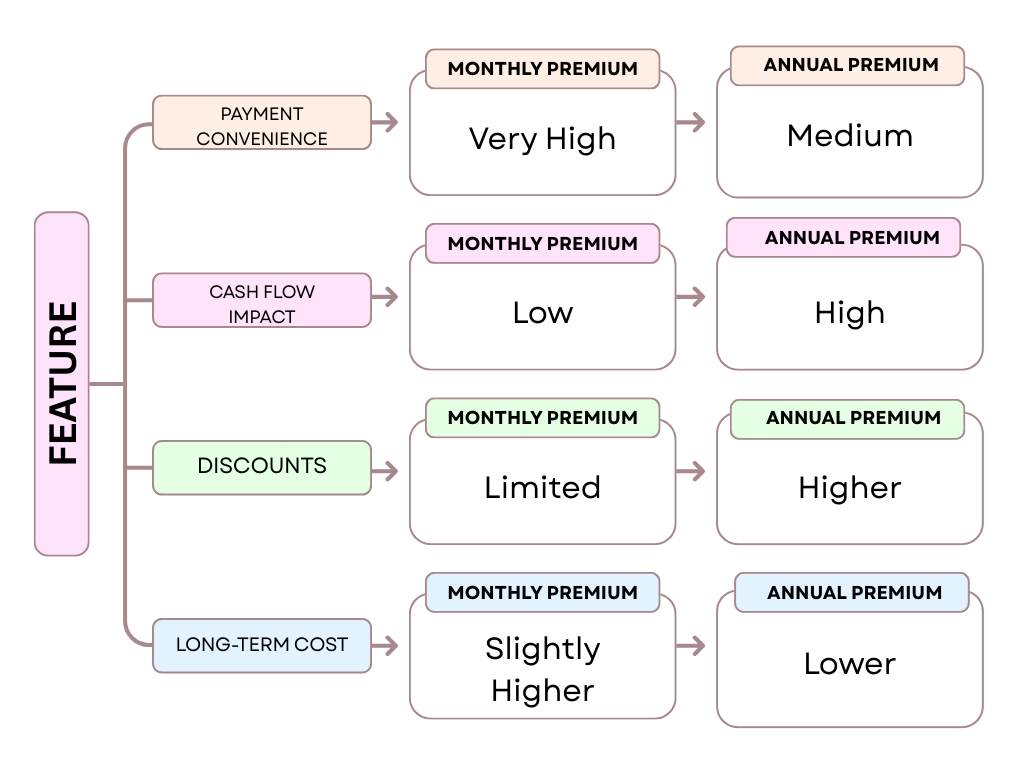

Monthly Annual Health Insurance Premium: Which Is Better?

When buying a health insurance policy, you can choose between paying premiums monthly or annually. Each option has its own advantages depending on your budget, cash flow, and long-term savings goals. Monthly payments offer flexibility, while annual payments often come with discounts and lower overall cost. The comparison below will help you decide which payment mode suits you best.

If affordability is your priority, monthly health insurance premiums work best. If saving money long-term matters more, annual payment is cheaper.

How To Reduce Your Health Insurance Monthly Premium Legally?

Here are proven strategies to lower your monthly medical insurance premium without sacrificing coverage:

1. Choose Higher Deductible

Opting for a voluntary deductible lowers your monthly health insurance premium significantly.

2. Buy at a Younger Age

Lock in lower premium rates early and enjoy lifelong renewability benefits.

3. Use Family Floater Plans

Instead of multiple individual policies, family floater health insurance reduces overall monthly premium costs.

4. Avoid Unnecessary Riders

Skip OPD or maternity riders unless you genuinely need them.

5. Maintain Healthy Lifestyle

Non-smokers and people with no lifestyle diseases enjoy lower premiums.

6. Use No Claim Bonus

Claim-free years increase your sum insured without raising premium, improving value per rupee.

How To Choose The Best Health Insurance Plan Based On Monthly Premium?

While choosing a medical insurance policy, don’t look only at the lowest monthly premium. Evaluate the overall value and coverage.

Check these key features:

- Sum insured adequacy

- Cashless hospital network

- Claim settlement ratio

- Room rent limits

- Sub-limits on diseases

- Waiting periods

- No Claim Bonus benefits

- Lifetime renewability

The best health insurance monthly premium plan balances affordability with strong coverage.

Is Monthly Health Insurance Really Worth it ?

Yes — especially if:

- You are a first-time insurance buyer

- You want flexible payments

- You have limited upfront budget

- You want uninterrupted medical coverage

Health insurance monthly premium plans ensure continuous financial protection while keeping your monthly expenses manageable.

Remember: A single hospitalization can wipe out years of savings, but a small monthly premium can prevent that.

Health Insurance Monthly Premium For Different Policy Types

1 . Individual Health Insurance Monthly Premium

Best for single adults, working professionals, and students seeking personal medical coverage.

2 . Family Floater Health Insurance Monthly Premium

Covers entire family under one sum insured, ideal for couples and young families.

3 . Senior Citizen Health Insurance Monthly Premium

Designed for people above 60 with higher premiums due to increased health risks but essential for retirement years.

4 . Critical Illness Insurance Monthly Premium

Provides lump-sum payout on diagnosis of serious illnesses like cancer, heart attack, or stroke.

Common Myths About Health Insurance Monthly Premium

- Low premium means good policy:

Low premium plans often come with low coverage, sub-limits, and higher out-of-pocket expenses. - Young people don’t need insurance:

Buying health insurance early locks in lower monthly premiums for life. - Monthly premium plans are very expensive:

They cost slightly more than annual plans but offer better affordability and payment flexibility.

Final Thoughts

Your ideal health insurance monthly premium depends on:

- Your age

- Family size

- Health condition

- City of residence

- Lifestyle habits

- Desired coverage amount

As a general rule:

- ₹500–₹800/month: Basic coverage for individuals

- ₹900–₹1,500/month: Family floater coverage

- ₹2,000+/month: Senior citizen medical insurance

Instead of choosing the cheapest plan, choose the most valuable plan within your budget because healthcare inflation rises faster than income growth.

5.0

Need advice from experts?

Health is tricky, and insurance trickier. But we’ll simplify it for you — for FREE! Book a call now. Limited slots available!